Evolution of Decentralized Exchanges

-

Evolution of Decentralized Exchanges

By Charles Liu, Vite Labs CEO

OTC — Stone Age of Trading

Digital assets (e.g. Bitcoin) caused unprecedented demand for ways to facilitate trade between people across borders. At first, this demand was fulfilled on social media platforms where asset holders would create posts or send messages within forums in order to discover trading counter-parties.

Commonly known as over-the-counter (OTC) trading, this method presents obvious problems including inefficiency, high risk of default and lack of effective pricing mechanisms.

As blockchain technologies grew in popularity, new digital assets emerged and more individuals entered the market. OTC trading could no longer keep up with this level of demand so exchanges emerged as designated spaces dedicated to trading.

Centralized Exchanges — Industrial Age of Trading

Centralized exchanges (CEX) gained popularity due to the increasing volume of digital assets and traders globally. Exchanges increased the efficiency of markets, since users could now congregate on common platforms to buy and sell orders that were quickly and automatically matched by the exchanges’ computer programs. In addition, exchanges decreased the risk of trader default by locking up the liquidity of counter-parties during trades.

Typically, a user would transfer their digital assets to a centralized exchange before conducting a trade. Their assets would be locked within the system at a predetermined exchange rate. Through a process called “matching,” the system would automatically find orders in the opposite direction and the exchange would conduct settlement of assets between counter-parties. During the matching process, both parties would be prohibited from moving their assets involved in the trade.

Although centralized exchanges were a welcome departure from OTC trading, they came with their own set of risks and flaws.

Security — Fundamental Flaw of Centralized Exchanges

Although centralized exchanges increased trade efficiency, eliminated default risk and provided an effective pricing mechanism, these benefits came with a price.

In order to ensure trade execution, centralized exchanges require users to deposit their assets. As such, these exchanges gained custody over a tremendous amount of assets, giving rise to serious security concerns. Users have to accept the risk that their exchange-held assets may be stolen and that these assets may be mismanaged by the exchanges. Meanwhile, exchanges must remain vigilant against potential hackers.

Ultimately, since assets go through a centralized authority, whenever an exchange is compromised, it is impossible to tell if stolen assets were looted by external hackers, misappropriated by the exchange or removed by exchange employees themselves.

Although exchange thefts are unlikely, to control security risks and asset misappropriation, exchanges impose restrictions on user redemptions (removing one’s money from an exchange). Any user of a centralized exchange knows that deposits are free and convenient, whereas redemptions involve many constraints (e.g. maximum redemption amounts, long processing times, manual verification requirements).

Monopoly — Original Sin of Centralized Exchanges

From a commercial perspective, centralized exchanges compete as individual corporate entities seeking profit maximization. Once an exchange becomes a monopoly, they exploit their position and charge exorbitant fees from projects looking to list on their exchange. This behavior threatens fair competition in the marketplace of digital assets, increasing both risks and costs for traders.

Many excellent projects in blockchain are organized around open communities, which often lack the capital to pay expensive listing fees. In contrast, mediocre projects that fundraise are able to pay these fees (sometimes over 50% of their fundraise) and use remaining funds for market manipulation to inflate their coin prices.

This kind of corrupt collaboration between exchanges and disreputable projects pose a serious risk for coin buyers, since these projects have neither the financial stability nor the technical capacity to achieve long term success. The result is a vicious cycle where bad coins simply crowd out good coins. This vicious cycle builds bubbles within digital asset markets, threatening the health of the entire blockchain industry.

Therefore, a coin buyer has a love-hate relationship with centralized exchanges. To summarize, here are the pain points for users:

- Lack of security of digital assets

- Bad user experience especially with registration and redemption

- No diversification of options since trading is limited to coins listed by the exchange

- Intransparent governance in rule-setting, listing fee remittance and matching logic

Decentralized Exchanges — Information Age of Trading

Decentralized exchanges (DEX) entered the spotlight due to problems associated with centralized exchanges.

The difference between centralization and decentralization can be summarized from a technology angle and from a governance angle.

In terms of technology, a decentralized exchange is a decentralized application (dApp) created on a public blockchain. Trustlessness and immutability are achieved through smart contracts.

In terms of governance, a decentralized exchange is open and driven by community participation; responsibilities are distributed within the community in a decentralized way.

In reality, many decentralized exchanges have been unable to achieve true decentralization from both angles. They either use centralized technologies and allow community participation in governance, or use decentralized technologies while keeping a centralized commercial and governance model.

So, what does a true decentralized exchange look like? What benefits can it offer users?

On-Chain and Cross-Chain — Decentralization from a Technology Angle

The technical stack of an exchange consists of two modules: 1) asset management 2) order matching. The former provides data storage, asset custody and trade settlement. The latter saves order book data and performs order matching.

A truly decentralized technology implements both modules with on-chain smart contracts. Users’ assets are held by smart contracts to safeguard against theft and misappropriation. Users freely redeem their assets without lengthy and complicated redemption processes. Order matching logic is dictated by smart contracts, which removes the risk of cheating behavior such as front-running.

Thanks to the advantages of blockchain, decentralized exchanges enjoy high uptime. At nearly any moment, a node is ready to provide services, hence guaranteeing the continuation of order matching and trade settlement. In the worst case scenario, a user can choose to run a node themselves in order to continue a disrupted trade and securely transfer assets to their wallet.

A completely decentralized solution requires strong performance from the underlying public blockchain alongside low cost of smart contract execution. To date, most public blockchains cannot meet both requirements. Many decentralized exchanges make the tradeoff by utilizing Layer 2 protocols to move low-frequency asset management modules on-chain while keeping high-frequency asset management modules off-chain. Although these solutions solve pressing asset safety issues through decentralization, the off-chain order matching logic reduces the extent of decentralization and subsequently increases the cost of developing and operating the decentralized exchange.

Lastly, the ability to support trading of many different assets (a.k.a. cross-chain) is another key differentiator for decentralized exchanges.

Ownership, Operation, Income Sharing — Decentralization from a Governance Angle

From a governance perspective, in a decentralized exchange, the rights of ownership, operations and income sharing belong to an open community rather than a single entity.

A centralized exchange determines trading hours and can freely change the rules of trading. The organizing entity decides who can trade and what they can trade. Value generated from trading belongs to the entity as income.

A decentralized exchange does not place ownership in the hands of one entity. All changes of trading rules are determined by consensus, via community voting or forking. The decentralized exchange does not select its users nor its trading pairs. The right to set trading fees belongs to the community. Similarly, value generated in a decentralized exchange is income for members of the community.

To date, both centralized and decentralized exchanges have launched some form of platform coin. Based on the economic model of these coins, one can clearly see the governance models of the exchanges.

If the platform coin exists mainly to offset transaction fees (with no other rights like voting power), then the coin is akin to a coupon or rebate. In this case, there is a centralized entity responsible for minting these platform coins for which holders are merely consumers who receive discounts.

Consider an alternative model in which the overwhelming majority of platform coins are owned by the community, which has the power to make decisions regarding exchange operations and is entitled to receive future proceeds from the exchange. In this case, the governance model is decentralized; by empowering the community to share in value generated by the exchange, users are incentivized to perpetuate the marketplace, which ultimately lowers transaction costs for traders.

Consider another feature in which the protocol of the decentralized exchange is made available to other exchange operators in order to increase liquidity. From a unified technology framework, all traders share a deeper order book, so rising tides lift all ships.

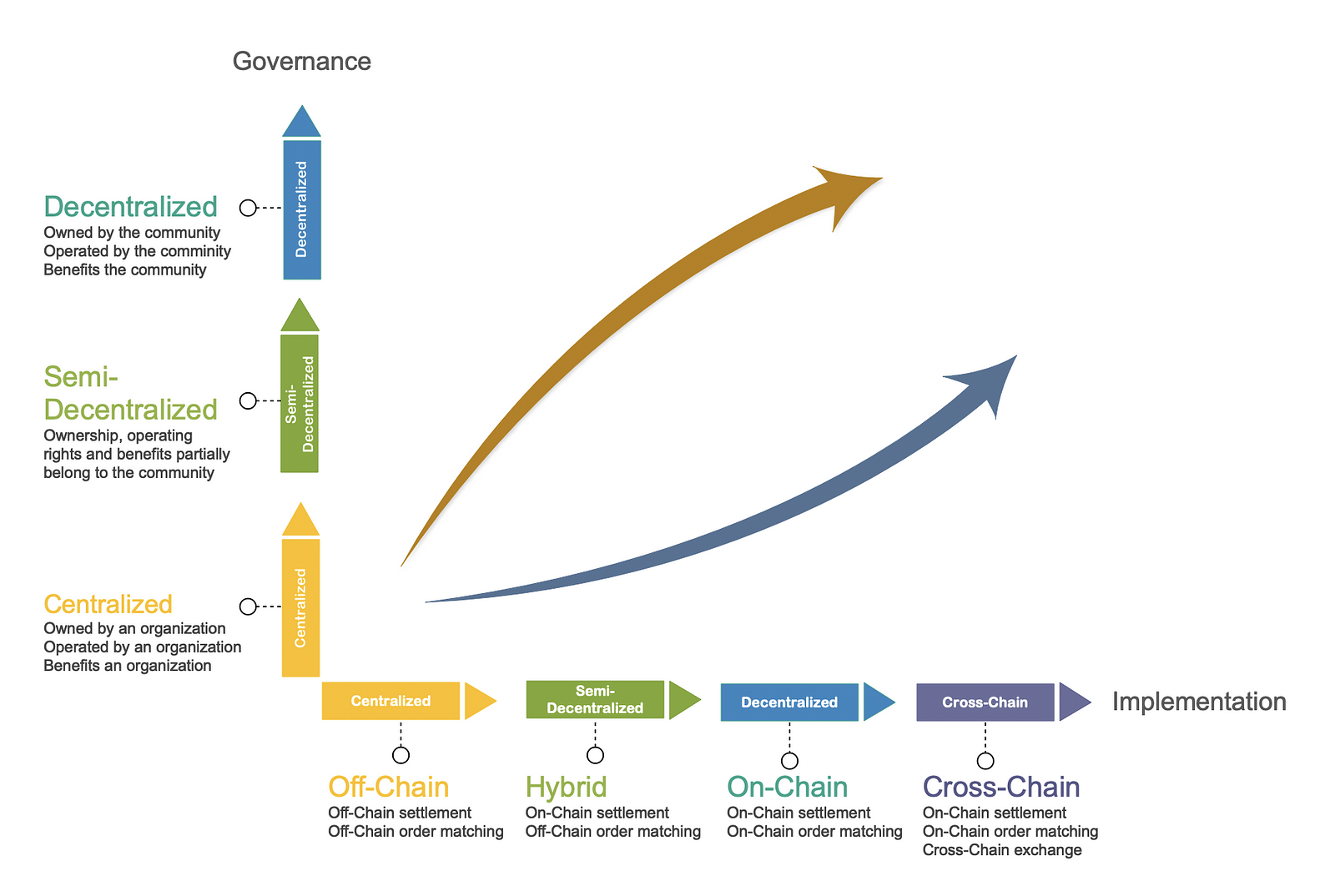

Path of DEX Evolution

The diagram shows the evolution of exchanges from the aforementioned two perspectives. The path to decentralization takes two different trajectories yet they both begin with centralized governance and technology, ending with decentralized governance and technology.

The evolution of exchanges

The evolution of exchangesChallenges

Many traders still prefer centralized exchanges over decentralized exchanges, which is understandable. Decentralized exchanges trail behind centralized exchanges in terms of user experience, with the biggest issues being 1) slow order matching 2) high transaction costs 3) insufficient liquidity. No user should tolerate trading confirmation times longer than 10 seconds or having to remit high fees for transaction cancellations. In short, users need the ability to quickly buy and sell digital assets at a low cost.

From a technology perspective, decentralized exchanges must solve for speed and cost. Such challenges are directly correlated to the performance of the underlying public chain. For this reason, many decentralized exchanges have opted to develop their own public blockchain.

Due to the differences in protocols, ledgers and consensus algorithms between public chains, solving the cross-chain liquidity problem of digital assets is a huge challenge. Although there are many cross-chain solutions, none have perfectly addressed this challenge.

Currently, the most viable option for decentralized exchanges to solve this issue is based on a cross-chain approach to notary, which is called “gateway.” The weakness of this model is its reliance on off-chain trust; this reliance prohibits true decentralization. Even if a mechanism for supervising, prioritizing and forming true consensus among different notaries exists, there is a possibility that the notary conspires to manipulate the system.

Another solution for cross-chain liquidity is the atomic swap. The atomic swap model is a peer-to-peer exchange of assets between different public chains, as opposed to a unidirectional asset transfer across the public chain. For example, to trade Bitcoin or Ethereum, one must find a counter-party willing to surrender a corresponding amount of ETH in exchange for BTC. Then, the ETH transfers to one’s wallet while one’s BTC is transferred to the counter-party’s wallet. In this way, the atomic swap is most suitable for OTC transactions but cannot satisfy on-chain order matching.

There is also a type of “isomorphic cross-chain” solution, used by projects like Cosmos and Polkadot, to improve interoperability between chains with existing protocols by designing a higher level protocol. The problem is that they cannot achieve “cross-chaining” between existing public chains, unless mainstream public chains such as Bitcoin and Ethereum are compatible with such higher level protocols. In the short term, this is a difficult reality to achieve because the cross-chain problem lies in the cross-protocol interaction and competition between public chains is essentially the competition between protocols. Therefore, accomplishing the goal of “cross-chaining” through a unified protocol is incredibly difficult.

Decentralized exchanges must provide sufficient liquidity incentives, which rely primarily on proper governance and incentive models. This requirement is often overlooked and it is the greatest shortcoming of current decentralized exchanges.

Strictly speaking, an exchange with decentralized technology and centralized governance should not be called a decentralized exchange. The decentralization of governance is far more difficult than the decentralization of technology. Whether it is the design of economic models, the establishment of communities or the development of trading ecosystems, full decentralization is a long process wherein traders, traditional exchanges, projects, market makers and crypto investors attempt to achieve a stable environment through ongoing competition and collaboration.

Therefore, a truly decentralized exchange should focus on building a complete trading ecosystem, coagulating the liquidity that was originally dispersed in different “centers” rather than trying to become a new “center.” This is the true meaning of decentralization.

Destination of DEX Evolution — Completely Decentralized Exchange

As public chains and governance models improve across the blockchain industry, all necessary pieces are available to build a commercially viable fully decentralized exchange. Users from traders to enthusiasts are looking forward to a new generation of digital asset exchanges that are decentralized from technology to governance. Vite Labs presents ViteX (Vite DEX), a product that brings us one step closer to the ideal.

- The exchange should be built on a high-performance, low-cost public chain with on-chain order matching and cross-chain capabilities.

- The exchange should have a fully open ecosystem that not only benefits the community, but rather, is “by the community for the community.”

- The governance model should benefit all participants within the ecosystem whether they are traders, operators, liquidity providers or blockchain projects.

ViteX is a decentralized exchange with a user experience on par with centralized exchanges. Assets are controlled by the user’s own private key and do not require complicated registration processes.

ViteX is an open platform that anyone can use to open their own trading zone as easily as opening a store on eBay.

The main role of ViteX operators is the “DEX operator,” which is similar to being an eBay store owner. These operators could be from centralized exchanges, blockchain projects, token funds or community leadership circles. Operators have their own trading zones and retain their own brands. They have the right to list trading pairs, set transaction fees and more. The operators’ brands and credits are critical to their success. For example, operators with strict listing standards and due diligence processes may be more likely to be promoted by users.

ViteX provides the infrastructure for community operated exchanges including smart contracts, websites, application programming interfaces (API) and software development kits (SDK). Operators either build their own websites based on the ViteX API or they connect with their own trading systems.

ViteX provides community incentives and decentralization through the VX platform token. There is no pre-sale nor pre-mining for VX, which ensures an equal playing field for all users. VX can be obtained through completing a transaction, opening a new trading pair, providing quotas for ViteX smart contracts, providing liquidity to ViteX, inviting new users and more. These rules are to be written into the smart contract as part of the protocol.

The ViteX platform is owned by VX holders and any changes to the protocols and rules must go through a voting process of VX holders. 100% of profits generated by ViteX will be distributed back to VX holders in proportion to their VX holdings.

ViteX is built on the Vite public chain. Vite is an asynchronous high performance public chain with smart contract capability, based on DAG ledger with Hierarchical Consensus mechanism. Transactions confirm within a second and there are no transaction fees. Vite offers multi-token support and cross-chain assets. Vite is designed for use cases like decentralized exchanges, which mandate a certain level of performance and stability.

Our intent is for ViteX to serve as a model that accelerates the evolution of decentralized exchanges across the industry. This movement would generate more business opportunities and bring prosperity to the digital asset ecosystem and to cryptocurrency traders.